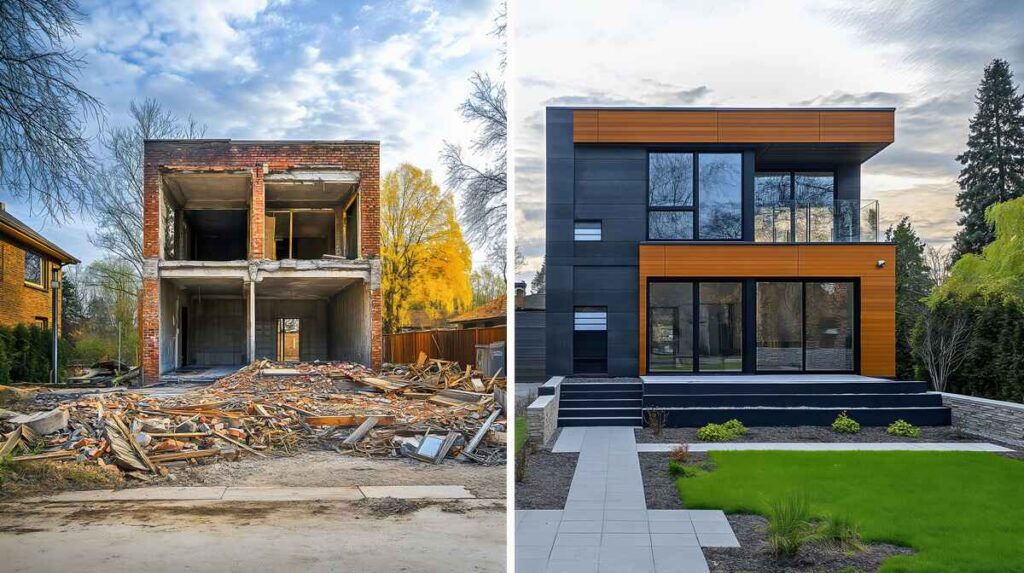

Using a Home Equity Line of Credit to install a pool

Tapping into the equity of your home to finance a large project such as building a pool can be possible thanks to a Home Equity Line of Credit (HELOC). In this article, I’ll review the process of financing home improvement projects such as installing a pool and this way you can figure out if using a HELOC is a good strategy for you. What is a Home Equity Line of Credit (HELOC) A Home Equity Line of Credit or HELOC for short, is a type of mortgage that works as a revolving line of credit. Unlike a regular fully amortized mortgage loan where you make a fixed monthly payment that goes towards principal and interest, a HELOC is a line of credit. This means that you have a limit but you may use as much as you want. Think of a HELOC as having a credit card. When you have a credit card, you also have a limit but from there, you access as much of it as you need. Your payment will be based on the interest rate and the balance you owe. Likewise, if you don’t have a balance, then you won’t incur and interest expenses or monthly payments. If you’re using a HELOC to finance installing a pool, you can draw as much as you want out of the line of credit up to the limit. 👉 Want to know if you qualify for a HELOC or check HELOC rates? Start here () Most Common HELOC Terms Available Home Equity Line of Credit lenders will offer different terms to choose from as far as for how long you can access the line and also, how long you have to repay it. The draw period is the period of time that you have to tap into the line of credit. The most common draw period that lenders offer is 10 years. Other terms available are 3 and 5 years. Sometimes, lenders can offer lower interest rates with lower draw periods terms. The repayment period is the time you have to pay the outstanding balance of the line of credit. The most common repayment periods with HELOCs are 20 and 30 years. The shorter the repayment period, the lower the rate lenders may be able to offer you. How do payments work on a HELOC? Unlike regular mortgages where a fully amortized principal and interest payment is required, the minimum HELOC payment required is interest only during the draw period. This means that if you only make the minimum required payment, your balance will not change. Thus, you’ll want to add another payment (known as a principal payment), in order to bring the balance down. For example, on a $100,000 balance HELOC with an interest rate of 9.99%, the interest only payment would be $823.50/month. Minimum credit scores and Requirements for Getting Approved for a HELOC Getting approved for a HELOC isn’t that different from qualifying for a regular mortgage — lenders still look at your credit score, income, debt, and available home equity. Let’s break down the most common qualifiers so that you know what would be expected from most lenders: Credit Scores Most lenders will want to see a minimum credit score of around 680, but if your credit is over 700, you’ll usually get better rates and terms. Don’t be surprised if certain banks will require you to have stronger scores, above 720. At Andes Mortgage, we offer HELOCs with credit scores as low as 680. Equity Position The amount of your equity will be important to get your HELOC approved. Depending on the lender or bank that you choose to go with, the maximum loan-to-value, will be anywhere between 80% and 90%. This means that the combined first lien amount and the HELOC may not exceed 80 or 90% of the value of your property. Your lender will determine if your property will need a full appraisal or an AVM or a Desktop Appraisal in order to gauge the value of your home. Debt to Income Ratio Your debt-to-income ratio or the maximum percentage of your gross monthly income that goes towards paying debt must be below 45%. You’ll need to show proof of income and a two-year employment or self-employment history. Things to Keep in Mind Before Using a HELOC Before you dive in (haha, get it?), here are a few important things to think about when getting a HELOC. Can you afford the additional payment? Pools are not cheap home improvements and if you finance the entire cost with a HELOC, you could be looking at another mortgage of $100,000 – $200,000 depending where you are. This is another payment that you’ll have on top of your current loan. Remember that nowadays property taxes and home insurance rates are on the rise. Consider how long you plan to stay in the home. If you’re planning to sell soon, you may not fully enjoy the benefits of your new pool—or have enough time to justify the cost. Your home is the collateral. A HELOC is secured by your house, which means missing payments could put you into foreclosure. A HELOC is a mortgage, and it is a lien against your house. Rates can fluctuate. HELOCs usually have variable interest rates. That means your monthly payment can go up or down depending on the market. Ask your lender if a fixed rate HELOC is a better solution or consider a cash out refinance or HELOAN instead. 👉 Want to know if you qualify for a HELOC or check HELOC rates? Start here () How Much Does It Cost to Install a Pool? Installing a pool isn’t cheap—but it’s also one of those upgrades that can genuinely change your lifestyle and even boost your home’s value when done right. On average, a standard in-ground pool can cost anywhere between $50,000 and $100,000, depending on the size, materials, and type of finishes you choose. If you’re going all-in with extras like waterfalls, lighting, or a spa

5 Ways to Lower Your Mortgage Payments (Insider info from a Mortgage Broker)

Want to lower your mortgage payment? I’m going to show you five strategies to save money on your monthly payments.

How to Access Your Home Equity to Buy Another Property

Whether you are wanting to buy another home because you’ve outgrown where you are or because you are wanting to invest in real estate, tapping into your home’s equity can be very advantageous. I’m going to go over how you can access the equity of your home to buy another property. In this article, I’ll also go over the pros and the cons of doing and some potential pitfalls that you need to be on the lookout for. Home equity mortgage rates. Start here. () First and foremost, what is home equity? Home equity is the difference between the current market value of a home and the outstanding balance on any mortgage or other liens against the property. For example, if your home is worth $500,000 in today’s market and your current mortgage balance is $300,000, you would have $200,000 worth of equity. Very simple. Loans to access Your home equity to buy another property When it comes to financing options to tapping into your equity to buy another property, there are three primary routes available. Cash-out Refinance This is a type of mortgage refinancing where you refinance your existing mortgage for an amount greater than the current outstanding balance. Because you are taking a new, bigger loan, the difference between what you owe, and the new mortgage would be your “cash out”. The new loan would substitute your current one and it would have a new interest rate, terms, and payments. For instance, if you have a mortgage for $150,000 and you did a cash out refinance for $200,000, your new mortgage loan would be for $200,000 and you would receive $50,000 as your cash out. How does a cash out refinance work? Uses of Funds: You can use the cash from the refinance for absolutely whatever you want. Most homeowner would use it for home renovations, debt consolidation, paying for education expenses, and of course, to buy another property to live in or invest in properties as investors. Repayment: You now have a new, larger mortgage to repay. Therefore, consider that before taking out the loan because odds are, your mortgage payment is going to increase. You should probably think twice to take on a much higher payment if you get too big of a loan. Likewise, if you take a new 30-year mortgage and your intention is to make the minimum payment only, you will pay more in interest compared to your current mortgage. To offset increasing your interest expense or having to restart paying on your home all over again, a cash out refinance allows you to adjust the repayment terms. With a refinance, you can take on a 20- or 15-year mortgage if your goal is to pay off your home faster. At Andes Mortgage, our clients are able to choose the term they want and even “odd years”. For instance, we are able to offer 23 or 18 year mortgages. Benefits: You get double the advantage on a cash out refinance when interest rates are lower than your current mortgage rate. Since 2021, rates have climbed to levels not seen in 20 years. For many people looking to do a cash out refinance, this presents the opportunity to lower the rate as well. On the other hand, one of the biggest disadvantages of a cash-out refinance is that if you have a low interest rate, this new loan will eliminate it as the mortgage would be paid off and replaced. Many homeowners who took out a mortgage from 2020-2022 have rates that have never been seen – the all-time lows. Consult with a mortgage or financial advisor to see if makes sense to take a new mortgage loan at a higher rate but if you don’t want to do that, then the next two options avoid paying off your current mortgage completely. Home Equity Line of Credit (HELOC) Over the last 3 years, the popularity of the HELOC’s has exploded due to so many homeowners not wanting to touch their current first mortgage but, still, wanting to access home equity to buy other properties. In short, a HELOC is a revolving line of credit that allows you to borrow against the equity in your home. This is a second mortgage, so it does not affect your current first mortgage. How does a HELOC work? Secured by your home: A HELOC is a 2nd lien on your home. The HELOC uses your home as collateral The amount you can borrow is based on the equity in the home, and that would now include your current mortgage and what the house is worth. I’ll explain on the next section what Loan to Value and Combined Loan To Value means. Revolving Line of Credit: A HELOC works similarly to a credit card. If you’ve had a credit card, then you know how a HELOC works. The same way with a credit card, you have a limit, and you can draw as much as you need from that limit. For example, if you have a HELOC limit of $100,000, and you need $50,000 to tap your equity to buy another home, then you only pay based on that balance. Don’t have a need to use it, and you want to keep the balance at zero? No problem, if you don’t have a balance, you pay any interest or have any payments. With a HELOC, you have what’s called as a “Draw Period”, typically 3-10 years to use it anytime you want, as much as you want. Normally, HELOC repayment terms are for 20 to 30 years. Variable Interest Rate: The majority of HELOCs have variable interest rates tied to a benchmark rate, such as the prime rate. Your rate will change once a month and when the Federal Reserve adjusts the Fed Funds Rate. From 2021 to 2024, the Federal Reserve aggressively raised interest rates to combat inflation. For those who have a HELOC, their rates went up as well. Hopefully in 2025 and beyond, we

FHA 203k Loan In Georgia | Renovation Mortgage Explained

You’re probably thinking about buying a home here in Georgia, but touring the same old cookie cutter overpriced new construction homes or resales in your area are simply not doing it for you. So you found a house that’s not in great condition but has some good bones on it in a great neighborhood and now you’re thinking – how can I buy this property and turn it exactly the way I want. This is where the FHA 203k loan comes in and, in this article, I’m going to tell you everything you need to know about using an FHA 203k renovation loan in Georgia. Today’s FHA 203k mortgage rates. Start here – () What is an FHA 203k Loan in Georgia? First things first, what exactly is an FHA 203k loan in Georgia? The FHA 203k loan is a subset of the FHA loan program. An FHA loan is a government-insured mortgage and one of the most popular loans for many homebuyers, especially first-time homebuyers. FHA loans are very attractive because they require a relatively small down payment, just 3.5% of the price of the house and it has some of the most forgiving credit requirements of any loan. For example, the FHA loan only requires a minimum 580 credit score to qualify. The difference between a regular FHA loan and an FHA 203k loan is that the 203k portion allows for the financing of the purchase and renovations or repairs into a single mortgage. Why is this so advantageous? Because the FHA 203k loan follows the same guidelines as a regular FHA mortgage. It has the same credit score requirements, debt-to-income ratio and most importantly, minimum down payment required. Follow along because I’m going to give you a real case scenario on how this loan would work on a rehab purchase. There are two types of FHA 203k loans in Georgia. Before we jump into a scenario, let’s highlight the two types of FHA 203k loans in Georgia. Standard 203k Loan The Standard 203k loan is used when you need extensive renovation in the home, including structural changes that cost more than $35,000. This would be the loan that you’d want to use if you are buying a “fixer-upper”. You will need to employ a HUD consultant and a General Contractor for the project when you are getting the standard 203k loan. Limited 203k loan The FHA limited 203k loan is designed for minor, non-structural or simple improvements in a home. You’ll use this loan if the total cost of your project is less than $35,000. Let’s say you’re looking to paint the house, maybe renovate a small bathroom, room, or use the funds for appliances. You would be suited for the 203k limited. Because the cost doesn’t exceed $35,000, HUD does not require the HUD consultant to oversee the project which will save you money. Get a mortgage quote. Start here: () How to qualify for an FHA 203k loan in Georgia? (If you are buying a house) There are three major requirements that you need to meet when you are looking to qualify for an FHA 203k loan in the state of Georgia. Let’s go over them. Credit score: 580 is the minimum credit score you’ll need Down Payment: 3.5% of the purchase price plus the cost of the rehab Debt-to-income ratio: FHA has a maximum 47% housing and 57% total debt-to-income ratio. Meaning, the total house payment cannot exceed 47% of your gross income and your overall monthly payments including the house payment cannot exceed 57% of your gross income. One last thing… OK maybe 4 major requirements. FHA loans are only for owner-occupied properties and the 203k loan is no different. If you want to use an FHA 203k mortgage for the purchase of a home in Georgia, you’ll need to occupy it as your primary home for at least 1 year. How to qualify for an FHA 203k loan in Georgia? (If you are a homeowner) You can use the FHA 203k if you are a homeowner as well. It would be a refinance of your current mortgage with the exception that you would increase your loan amount in order to do the renovations that you need. These are the requirements: Credit Score: 580 is the minimum credit score you’ll need Loan to Value: The maximum LTV allowed is 96.5% BUT this is based on the After Repair Value (more on this later) Debt-to-income ratio: 47% housing and 57% total debt to income ratio What types of renovation projects are eligible for the FHA 203k Loan? You are going to be really surprised about the amount of work that you can do with an FHA 203k loan for your home in Georgia. I’m just going to highlight some of the most common ones here: Structural alterations and reconstruction Remodeling of kitchen, bathroom, bedrooms, etc. Adding a bedroom or extra room Closets Changes to the appearance of the property Elimination of health and safety hazards Adding energy efficient improvements such as solar panels Roofing, gutters, downspouts Major landscaping work Electrical, plumbing, wells and/or sceptic systems HVAC replacements Accessibility or modifications for elderly or disabled individuals Adding or repairing decks, patios, porches The FHA 203k loan can help you do a whole lot to a house but it does not allow for luxury items such as: Swimming pools Hot tubs, saunas Outdoor kitchens Or just about anything that doesn’t improve the house itself (non-essential). Real life scenario for an FHA 203k loan in Georgia Our client purchased a home that needed extensive repairs in Atlanta in 2024. The price of the house was $230,000 and after talking to a General Contractor, they came up with a list of items that they wanted to tackle. The total amount of the repairs was $70,000. With the 203k loan, our client had an “adjusted” purchase price of $300,000. Since the adjusted price was $300,000, her down payment of 3.5% came out to $10,500. We financed $294,567 after

Refinance To Pay Off Debt: Is It Right For You?

With credit card interest rates averaging well over 24% in 2024, one increasingly popular option is refinancing a mortgage to pay off debt. This strategy can offer significant benefits if you are looking to consolidate debt, but it’s crucial to evaluate whether or not it makes sense for your unique financial situation. See today’s refinance rates. Start here – () What is Refinancing to Consolidate Debt? Mortgage Refinancing involves replacing your existing home loan with a new one, usually to secure better terms or rates. When it comes to consolidating debt, there are two primary types of refinancing to consider: Cash-Out Refinance Allows you to borrow more than you owe on your home and take the difference in cash to pay off other debts. For example, if you owe $300,000 on your mortgage and you’d like to pay off $50,000 in other debt such as credit cards, auto loans, or other loans, you would take out a $350,000 mortgage. Rate and Term Refinance Focuses on obtaining a lower interest rate or changing the loan terms without taking out additional cash. Situations where refinancing might be beneficial include high-interest debt consolidation, lowering monthly payments, or securing a better interest rate. What do you need to get a cash out refinance to pay off your debt? Having sufficient home equity is vital when considering refinancing. The Loan-to-Value (LTV) Ratio is a key metric lenders use to assess your eligibility. For FHA and conventional loans, the maximum loan amount you can take is 80% of your property’s value (80% Loan-to-Value). Meanwhile, VA loans allow you to take up to 100% of your property’s value. Home Equity Having sufficient home equity is vital when considering refinancing. The Loan-to-Value (LTV) Ratio is a key metric lenders use to assess your eligibility. For FHA and conventional loans, the maximum loan amount you can take is 80% of your property’s value (80% Loan-to-Value). Meanwhile, VA loans allow you to take up to 100% of your property’s value. Credit Score Lenders typically require a credit score of at least 620 to approve a cash-out refinance. However, the better your credit score is, the more favorable terms you can secure on your new loan. A good credit score also demonstrates responsible financial management and makes you less risky as a borrower. Note: If you don’t have an excellent credit score or enough home equity, consider applying with a co-borrower who meets these requirements. Debt-to-Income Ratio Your debt-to-income (DTI) ratio is another factor that lenders consider for refinancing. It is the percentage of your monthly income that goes towards debt payments, including your new mortgage payment. Most lenders prefer a DTI of 45% or lower, but some may go up to 57%. Keeping a low DTI shows you have enough income to cover all your debts and are less likely to default on your loan. Get a mortgage refinance quote. Start here: () Qualifying for a debt consolidation refinance Credit Score and Debt-to-Income Ratio (DTI) Lenders typically require a good credit score and a manageable Debt-to-Income Ratio (DTI). A higher credit score can help you secure better terms, while a lower DTI shows lenders you can manage your new mortgage payments alongside your existing debt. Appraisal and Home Value A home appraisal determines your property’s current market value, which influences your loan terms and eligibility. Higher home value can lead to better refinancing conditions. Costs Associated with Refinancing Refinancing comes with various costs, including: Closing Costs: Fees for processing the new loan Insurance Premiums: Homeowners insurance and potentially PMI Application and Origination Fees: Costs associated with applying for and originating the new loan Third Party Costs and Taxes: Fees for services like appraisals, title searches, and recording fees Mortgage Refinance Options Conventional Cash-Out Refinance This option allows you to take out a new conventional mortgage for more than you owe and use the extra cash to pay off other debts. Benefits include potentially lower interest rates compared to other debts, and eliminate mortgage insurance if you are currently paying PMI or have an FHA loan. FHA Cash-Out Refinance With an FHA loan, you can also tap into your home’s equity and pay off other debts. This type of refinancing requires mortgage insurance, which could offset some of the savings on interest rates. However, FHA loans allow homeowners with lower credit scores and high debt to income ratios to be able to qualify. VA Cash-Out Refinance The VA Cash-Out Refinance is a beneficial option available to veterans and active-duty service members, allowing them to convert their home equity into cash. This program not only enables borrowers to pay off existing debts but also provides an opportunity to secure a lower interest rate on their mortgage. Unlike FHA loans, VA loans do not require private mortgage insurance (PMI), which can result in significant savings. VA loans allow veteran homeowners to tap up to 100% of the property’s value, making it the only loan that allows it. Non-QM Cash-Out Refinance Non-Qualified Mortgage (Non-QM) cash-out refinance options provide flexibility for borrowers who may not meet the traditional mortgage criteria. These loans cater to those with unique financial situations, such as self-employed individuals or those with irregular income streams, allowing them to leverage their home equity. Non-QM loans include but are not limited to Bank Statement loans, P&L loans, DSCR loans, 1099 loans and more. Alternative loans to access equity from your home Home Equity Lines of Credit (HELOC) A Home Equity Line of Credit (HELOC) allows homeowners to borrow against the equity in their homes in the form of a second mortgage. Unlike traditional loans, a HELOC operates similar to a credit card, providing a revolving line of credit that can be utilized as needed, up to a predetermined limit based on the homeowner’s equity. This flexibility enables borrowers to tackle various expenses, such as home renovations, educational costs, or even unexpected emergencies. Typically, HELOCs come with variable interest rates, which can affect monthly payments. Additionally, many lenders offer interest-only payment options

Everything You Need to Know About the Empowered Down Payment Assistance (DPA) Grant

I want to tell you about a one of the best down payment assistance programs that I’ve seen in the last few years, the Empowered Down Payment Assistance grant. The Empowered Down Payment Assistance (DPA) grant offered by Mortgage Brokers thanks to Equity Prime Mortgage, a wholesale mortgage company is designed to help first-time homebuyers, government employees, and medical professionals and others, getting a home more affordably. See today’s mortgage rates in for first-time homebuyers in Georgia. Start here – () What is the Empowered Down payment Assistance Grant? The Empowered down payment assistance grant provides qualified homebuyers with either 2% or 3.5% for down payment assistance. This assistance can be used for either the down payment, closing costs or combination of both when purchasing a home. Borrowers have to qualify for an FHA loan as the main financing to get access for the Emplowered DPA grant. FHA loans require a 3.5% down payment. Essentially, this means that eligible buyers can purchase a home with little to no money coming out of their pocket for the down payment. More about this later in this post. Who Can Benefit from the Empowered DPA Grant? This grant is specifically targeted at: First-Time Homebuyers: If this is your first time purchasing a home, you could qualify for this valuable assistance. Government Employees: Both current and retired State or Federal Government employees are eligible. Educators Civil servant in a state or local municipality Medical Professionals: Whether you’re currently employed or retired from the medical field, this grant could be for you. Borrowers who live in an underserved census tract One of the best things about this grant is that borrowers do not have to be first-time homebuyers like most other down payment assistance programs. So as long as they can meet one of the criteria above, they may qualify. Find the best first-time homebuyer program in Georgia for your situation. Start here: () Key Benefits of the Empowered Down Payment Assistance Grant 1. Financial Relief One of the significant hurdles in buying a home is coming up with a substantial down payment. With the Empowered DPA grant offering 2% or 3.5% down payment assistance, this initial financial strain is lifted, making homeownership more accessible. 2. Forgivable Grant The grant provides up to 3.5% of the purchase price, which does not have to be repaid after you’ve made at least 6 months of payments on your mortgage. Most down payment assistance programs require repayment which makes this one a better option. 3. You do not need to be a first-time homebuyer to qualify As mentioned earlier, the Empowered DPA grant is open to eligible borrowers who meet one of the criteria listed above. This makes it a great option for those who may have previously owned a home and are looking to purchase again. 4. Helps You Build Equity Faster By providing assistance with your down payment which doesn’t have to be repaid, the grant essentially helps you free up equity in your home. 5. Making Homeownership Affordable Overall, the grant helps make buying a home more affordable, enabling more people to step into the roles of homeowners without the usual financial stress. What is the minimum credit score to qualify for the Empowered Down Payment Assistance grant? The Empowered Down Payment Assistance Program requires a minimum credit score of 620. Also, the maximum debt to income ratio to qualify is 49% as of 2024. How to Apply for the Empowered DPA Grant The grant is available through mortgage brokers like us. Here at Andes Mortgage, we can help you determine if you are eligible for the grant and guide you through the application process. If you want to check your eligibility, simply click this link to get started. Start your Empowered Down Payment Assistance Program Application In conclusion The Empowered Down Payment Assistance (DPA) grant is a valuable resource for those looking to purchase their home. By reducing the initial financial burden, offering a forgivable grant, and working in conjunction with the FHA loan, this grant makes homeownership a reachable goal for many. Ready to take the next step? Learn more about how the Empowered DPA grant can help you achieve your dream of homeownership. [Book a consultation with one of our experts today!] Find a first-time homebuyer grant in your area. Start here.

DSCR Loans Explained – What you need to know.

In this article, I’m going to teach you everything that you need to know about DSCR loans and how they can help you purchase investment properties. This somewhat “little-known” loan can be the tool you need to kick off your real estate investment career or help you increase the size of your real estate portfolio rapidly. Let’s dive in. Check out what first-time homebuyer program you qualify for in – Updated on What are DSCR loans? Let’s make this simple. DSCR loans are a type of mortgage financing used in investment real estate including residential, commercial and even industrial. DSCR stands for debt service coverage ratio and it’s a way to measure the cash flow of an investment property. DSCR loans are just mortgages that use this ratio as a factor in determining loan eligibility and terms. How to calculate the DSCR of an investment property? The best and easiest way to calculate the debt service coverage ratio for a DSCR loan is by dividing the rental income of the property by the monthly house payment. This payment will include the principal and interest, taxes, insurance and HOA if applicable. The result is a number that shows how many times over the income will cover the property’s payment. For example, if the expected rent of a property is $3,000/month and the payment is $3,000/month, the ratio is 1. If the rental income is $3,000/month and the payment is $2,500/month, the DSCR would be 1.2. In general, most mortgage lenders require a minimum DSCR of 1, sometimes even less, to consider lending on an investment property. At Andes Mortgage, we have DSCR loans were the ratio can be as low as 0.75 and sometimes, even no ratio is required. But remember, most lenders will want to see that the property’s income can at least cover the payment. How DSCR is Calculated The DSCR is calculated by dividing the net operating income (NOI) by the total debt service. The formula is: DSCR= Rental Income / Property’s Payment For example, if a property generates $3,000 a month in rents and the payment is $2,500 a month, the DSCR would be 1.2. Why DSCR Matters The DSCR is crucial because it indicates the financial health of a property or business. Lenders use this ratio to determine the risk of default. A higher DSCR suggests that the borrower is more likely to meet their debt obligations, while a lower DSCR indicates higher risk. With that being said, the higher your DSCR ratio is, the lower your interest rate will be. Likewise, if your DSCR is low or under 1, you should expect higher interest rates. Looking for investment property interest rates in – Updated on . Start here. Differences between a DSCR loan vs a Conventional Mortgage At this point, you’re probably wondering why this loan over a more commonly known loan such as a conventional mortgage. Unlike traditional mortgages, where your personal income is required, DSCR loans only take into consideration the income that the investment property generates. This is huge for investors, self-employed borrowers, or even salaried borrowers who want to acquire multiple properties in a real estate portfolio. With conventional mortgages, it becomes increasingly more difficult to qualify when multiple properties come into play, and personal income can’t cover the mortgage payments. Since DSCR loans don’t look at your personal income to qualify, you can purchase as many properties as you wish, so as long as you meet the minimum down payment and credit requirements and like we said before, the DSCR ratio is sufficient for the lender. The Advantages of DSCR Loans Flexibility: Traditional mortgages can be restrictive in terms of how many properties you can acquire because of the need to show personal income. DSCR loans offer greater flexibility as they focus on the investment property’s income rather than the borrower’s personal income. Easier Approval Process: Since these loans do not require a borrower’s personal income, the approval process is usually quicker and less stringent than traditional mortgages. Higher Loan Amounts: With conventional mortgages, lenders tend to limit how much they will lend based on a borrower’s debt-to-income ratio (DTI). With DSCR loans , lenders can extend credit into the millions of dollars. Buying real estate properties under an LLC with DSCR Loans Another significant advantage of DSCR loans is the ability to purchase properties under a limited liability company (LLC). This option offers several benefits, such as: Asset Protection: By purchasing properties under an LLC, your personal assets are protected from any potential liabilities that may arise from the property. Tax Benefits: LLCs offer tax advantages, including the ability to deduct expenses related to the investment property and avoid paying self-employment taxes. Easier Management: Operating under an LLC can make managing multiple properties more manageable, especially when it comes to bookkeeping and record keeping. Blanket Loans with DSCR Loans If you have multiple properties or are you looking to purchase multiple and want to wrap them under one loan, DSCR can be a solution. With a DSCR loan, you can get a “blanket loans” or “portfolio loan”, which involve financing multiple properties on a single loan. This type of loan offers several benefits: Simplified Financing: Instead of securing individual loans for each property, a blanket loan allows the borrower to manage and make payments on all properties under one loan. Lower Interest Rates: With a blanket loan, you may be able to negotiate lower interest rates compared to what you would get if you had multiple separate loans. Lower closing costs: Having one loan instead of multiple loans means fewer closing costs, saving you money in the long run. This can save you a lot especially if you are looking to refinance multiple properties and you are staring at tens of thousands in closing costs. Looking for investment property interest rates in – Updated on . Start here. Qualifying for a DSCR Loan To qualify for a DSCR loan, borrowers must meet certain criteria: Credit score To

What You Need to Know About Mortgage Discount Points

When it comes to getting a mortgage, whether you are buying a home or refinancing, you may come across different lingo that can be pretty confusing to understand. One of those terms that you may encounter is called “discount points” or “points”. Today, we will dive deeper into understanding mortgage points and how they can impact your overall financing. See today’s mortgage rates in Atlanta, GA. Start here:() What are Mortgage Points? Mortgage points, also known as discount points, are fees paid directly to the lender at closing in exchange for a reduced interest rate. Essentially, they are prepaid interest on your mortgage. One point equals one percent of your loan amount. For instance, one point on a $300,000 loan would be $3,000. To make it more simple to understand, one point equals to one percent of the loan amount that you are acquiring. As a rule of thumb, for every 1 point you pay, you should expect your interest rate to be reduced by anywhere between 0.125 to 0.25%. Two types of Points – Discount Points vs Loan Origination Points It’s important to differentiate between discount points and loan origination points. Discount points are used to lower your interest rate, while loan origination points are a fee charged by the lender for processing and underwriting your loan. Depending on your credit scores, loan type, down payment and other factors, the costs of these points will differentiate. For example, if you have great credit scores and a sizable down payment, the cost of getting a lower interest rate will be substantially lower than if you had low credit and a low to no down payment. Likewise, both your credit scores, down payment, loan type and other factors will affect the mortgage origination points. Again, these being a cost for originating your loan in certain loans. For someone who is well qualified, the cost will be lower than a buyer who has minimum qualifications. What is the PAR Rate and How is it Different from the Interest Rate? In order to understand the value and the meaning of points, you have to know what the “PAR” rate is. The PAR rate, or “par value”, is the base interest rate that a borrower can receive without paying any points. This means if you don’t pay any points upfront, your interest rate will be equivalent to the PAR rate. Let’s call it the “free” interest rate to you. You are not paying anything to acquire this rate. In other words, the PAR rate is the true interest that you qualify for based on many factors, most importantly, market conditions, loan type, loan amount, loan to value, debt to income ratio and credit scores. There are many other factors that influence your PAR rate but these are the most important ones. Now, when it comes to mortgages, your lender may offer you an interest rate that is either above or below the PAR rate. In this case, if you want to secure a lower interest rate below PAR, you can pay discount points upfront to achieve it. On the other hand, if you are willing to pay a higher interest rate than PAR, you may receive lender credits that will cover some or all of your closing costs. It’s important to keep in mind that these options have an impact on your overall mortgage payment and the total cost of the loan. Find mortgage programs in Atlanta, GA. Start here: () Why should you pay discount points? Paying discount points can be a great way to save money over the life of your loan. For example, these are some of the main benefits of discount points: Lower monthly payments: With a lower interest rate, your monthly mortgage payments will be reduced compared to not acquiring discount points. Save money over the long term: By paying upfront for a lower interest rate, you can save thousands of dollars over the life of your loan. Below, I’ll show you an example of how discount points can help you save over the loan term. It’s important to do the math and see if it makes sense for your specific situation. Tax-deductible: In some cases, you may be able to deduct the cost of discount points on your taxes. This can potentially provide additional savings during tax season. How Discount Points Can Save You Money – 30-Year Mortgage Example Let’s take a look and see how discount points can help you save money when taking out a 30-year fixed rate mortgage for $300,000. Over the life of a 30-year mortgage, that one discount point can save you a total of $32,303 in interest payments! Example 2: How Discounts Points Can Save You Money on a 15 Year Mortgage This time around, let’s assume that you are more concerned with paying off your loan faster and saving on interest payments. As you can see, you would save nearly $14,000 in interest payments over the 15 years but also have a reduced payment by $77.40. In both examples, it’s apparent that you would have more savings by investing in discount points than not. What are Origination Points and How are They Different from Discount Points? As mentioned earlier, origination points are different from discount points. While discount points are paid upfront to lower your interest rate, origination points are a fee that the lender charges for processing and underwriting your loan. This fee is usually a percentage of the total loan amount and can vary depending on the borrower’s credit score, loan type, and down payment. Unlike discount points, origination points cannot be used to lower your interest rate. Instead, they are a cost that is added on top of your mortgage amount. Who Benefits from Mortgage Points? Mortgage points typically benefit long-term homeowners. If you plan to stay in your home or keep the mortgage for a long time, buying points to lower your interest rate can save you money over the life of your loan. However, if

Navigating FHA Loans – Expert Tips to Help you Through the Process

So, you’re in the market for a new home and you just happened to stumble upon FHA loans. Coincidence? I think not. Let me tell you, navigating FHA loans can be a game-changer for homebuyers like you. Forget those traditional loans with their strict requirements and sky-high down payments. FHA loans are here to save the day. With their low down payment options and flexible credit requirements, you can finally say goodbye to renting and hello to homeownership. But don’t just take my word for it. In this guide, I’ll show you how to navigate the ins and outs of FHA loans, from understanding the benefits to meeting the requirements. Brace yourself, my friend, because buying a home just got a whole lot easier. Understanding FHA Loans To understand FHA loans, you need to grasp the basic requirements and benefits. Let’s start with FHA loan eligibility. Unlike conventional loans, FHA loans are more lenient when it comes to credit scores and down payments. So even if you don’t have a perfect credit history or a hefty down payment, you still have a shot at homeownership with an FHA loan. It’s like a lifeline for those who may not qualify for a traditional mortgage. Now, let’s talk about FHA loan limits. These limits determine the maximum amount you can borrow for your mortgage. The idea behind these limits is to ensure that FHA loans are accessible to a wide range of borrowers, regardless of the cost of housing in their area. The limits vary by county, so it’s crucial to check the limits in your specific location. FHA loans have revolutionized the homebuying process for many Americans. They offer a lifeline to those who may not meet the strict requirements of conventional loans. With its lenient eligibility criteria and reasonable loan limits, FHA loans make homeownership a possibility for many who thought it was out of reach. So, if you’re dreaming of owning a home but don’t have a perfect credit score or a large down payment, don’t despair. FHA loans are here to help you make that dream a reality. Benefits of FHA Loans You can enjoy numerous benefits with FHA loans. One of the biggest advantages is the streamlined application process. Unlike traditional mortgages that can be riddled with paperwork and red tape, FHA loans offer a simplified and efficient process. This means less hassle for you and a quicker turnaround time. Another benefit of FHA loans is the lower down payment options. While conventional loans typically require a hefty down payment of 20% or more, FHA loans allow you to put down as little as 3.5% of the purchase price. This lower down payment requirement can make homeownership more attainable for individuals who may not have a large amount of savings. Additionally, FHA loans offer more lenient credit requirements compared to conventional loans. If you have less-than-perfect credit, you may still be able to qualify for an FHA loan. This flexibility can be a game-changer for many potential homebuyers who may have been otherwise shut out of the mortgage market. FHA Loan Requirements Meeting the FHA loan requirements is essential for obtaining financing for your home purchase. Let’s be honest, getting a loan can be a daunting task. But with FHA loans, the requirements are not as strict as with conventional loans. That’s why they are so popular among first-time homebuyers. When it comes to FHA loan qualifications, they are relatively lenient. You don’t need a perfect credit score or a massive down payment. In fact, the minimum credit score required for an FHA loan is 580, which is much lower than what most traditional lenders require. This means that even if you’ve had some financial hiccups in the past, you still have a shot at getting approved. However, don’t think that FHA loans are a free pass. You still need to meet certain criteria. For instance, you must have a steady income and be able to show proof of employment. You also need to have a debt-to-income ratio within the acceptable range. These requirements are in place to ensure that you can handle the financial responsibility of homeownership. Comparing FHA Loans to Other Loan Types Because FHA loans have more lenient requirements, it’s important to compare them to other loan types to determine which option is best for you. Let’s face it, not all loans are created equal. So, let’s break it down for you and compare FHA loans to two other popular loan types: conventional loans and VA loans. Here’s what you need to know: Now that you have a clearer picture of how FHA loans compare to other loan types, you can make an informed decision that suits your needs and financial situation. Remember, it’s all about finding the loan that works best for you. Navigating the FHA Loan Process To successfully navigate the FHA loan process, it’s important to understand the key steps involved in obtaining this type of loan. Let’s start with the FHA loan application. This is where you provide all the necessary information about your financial situation, employment history, and credit score. The application process may seem daunting, but don’t worry, it’s just a formality to get the ball rolling. Once your application is submitted, the FHA loan approval process begins. This is where the lender evaluates your application, reviews your credit history, and determines if you meet the requirements for an FHA loan. It’s important to note that this process can take some time, so be patient. During the approval process, the lender will also assess the property you intend to purchase using the FHA loan. They will conduct an appraisal to ensure that the property meets the minimum standards set by the FHA. If your application is approved and the property passes the appraisal, congratulations! You’re one step closer to obtaining your FHA loan. The final step is closing the loan, which involves signing the necessary documents and paying any closing costs. Navigating the FHA loan process can

How to Remove Your PMI Without Refinancing

Are you tired of paying for private mortgage insurance (PMI) every month? You’re not alone. Many homeowners are looking for ways to remove their PMI and save money on their monthly mortgage payments. The good news is that there are a few options available to help you get rid of your PMI without having to refinance your mortgage. Today, I’m going to show you how to remove your PMI without refinancing, so you can keep more money in your pocket each month. See today’s mortgage rates in , . Start here () What is Private Mortgage Insurance (PMI)? Private mortgage insurance is a type of insurance that protects the lender in case you default on your mortgage payments. It’s usually required if you have less than 20% equity in your home, and it can add hundreds of dollars to your monthly mortgage payment. PMI is not to be confused with homeowners insurance, which protects you in case of damage or loss to your property. What is the process of removing your PMI without refinancing? First, you’ll need to contact the servicer of your mortgage. This is the lender that you make your payments to. You will want to speak with one of the customer service representatives and formally request for cancellation of your PMI and provide evidence that your loan to value has reached 80% or lower. This can be done through a recent appraisal, statement showing extra payments made towards the principal balance, or any other documentation requested by your lender. Once approved, you should see a reduction in your monthly mortgage payment What is the timeframe to remove your PMI without refinancing The whole process should take less than 3 weeks. It’s important to note that every lender may have their own specific requirements and procedures for removing PMI. It’s best to contact them directly and inquire about their process. Keep in mind that even if you do remove your PMI, there may be other fees associated with it such as an appraisal fee or processing fee. Be sure to factor these costs into your decision-making process. Remove your PMI if your home value increaes If your home value increases, you may have more options to remove your PMI without refinancing. You can request a new appraisal or use a current appraisal that shows the increased value of your home. If the LTV ratio is now below 80%, your lender may approve the removal of PMI. However, make sure you check with your lender first because often times, even if you have enough value in your home to remove your PMI, the lender may first require that you have your mortgage for at least 1 or 2 years. You will also be required that you have shown an on-time payment history as well. Can you qualify for a mortgage without PMI in , ? Start here () How to remove the FHA PMI FHA loans also require PMI, but their process for removal is different. If you have an FHA loan and made a down payment of less than 10%, you will be required to pay for PMI throughout the entire term of the loan. However, if you made a down payment of 10% or more, then after 11 years, your PMI will drop off automatically. However, most FHA borrowers are not eligible to request a removal of their PMI simply because their Loan to Value reaches 80% or less. For the most part, refinancing into a conventional loan is the only way to remove PMI on an FHA loan. So, how can you remove your PMI without refinancing? Here are some options to consider: By making a larger down payment One way to avoid PMI altogether is by making a larger down payment when purchasing your home. If you put down 20% or more, you won’t be required to pay for PMI. This may not be a feasible option for everyone, but it’s worth considering if you’re still in the process of buying a home. Request a PMI cancellation If you already have PMI on your mortgage, you can request to have it cancelled once you reach 20% equity in your home. This means that your loan-to-value ratio (LTV) has dropped to 80% or less. Keep in mind, though, that this is not an automatic process and you’ll need to contact your lender to initiate the request. Make extra payments Another way to reach the 20% equity mark faster is by making extra payments towards your mortgage. This will help you pay off the principal balance of your loan quicker, thereby increasing your equity and potentially reaching the 20% threshold sooner. Improve your home’s value You can also try to increase the value of your home by making improvements or renovations. This may not be a quick solution, but it could potentially increase your home’s worth and lower your LTV ratio. Get a new appraisal If you believe that your home’s value has increased significantly since you purchased it, you can request a new appraisal to prove this to your lender. If the appraisal shows that your LTV is now below 80%, you may be able to cancel your PMI. How much mortgage do you qualify for in , ? Curious? Start here () So, how can you remove your PMI without refinancing? Here are some options to consider: A loan is eligible for PMI cancelation when all the below criteria are satisfied: The loan-to-value ratio (LTV) has reached 80.0% of the original value of the loan. The original value of the loan is defined as the lesser value of the purchase price and the original appraised value The LTV is calculated by dividing the unpaid principal balance (UPB) by the original value If the LTV has not reached 80.0%, there is the option to pay down the loan. The borrower can request the amount from the MI department of their servicer to ensure the accuracy of the pay-down amount. The property has increased in value The lender